Select a language

As of October 2022, the Airbus A320-200 was the world’s second most popular aircraft. It accounts for 11.6 percent of aviation carbon emissions, second only to the top-seller Boeing 737-800. So how is it that producing the Airbus aeroplanes which are flying you from Paris to Helsinki, or from Dublin to Izmir, is marketed as a “green” business to investors?

The contradiction stems from flawed legal safeguards put in place by the European Union (EU) in a loophole that allows so-called 'green funds' to invest in activities causing climate damage, while officially vouching for the public good.

These funds are mostly managed by banks alongside pension funds and insurance companies. They are commonly referred to as "ESG" financial products, since they aim to address environmental, social and governance issues, in addition to ensuring profits for investors.

However, the managers of these funds, which are marketed as environmentally (or socially) responsible, invest in the world's largest carbon or greenhouse gas (GHG) emitting companies in an attempt to capitalise on the success of green financial markets in Europe. As a result, they are driving investor money into “greenwashing”: the “act or practice of making a product, policy, activity, etc. appear to be more environmentally friendly or less environmentally damaging than it really is”.

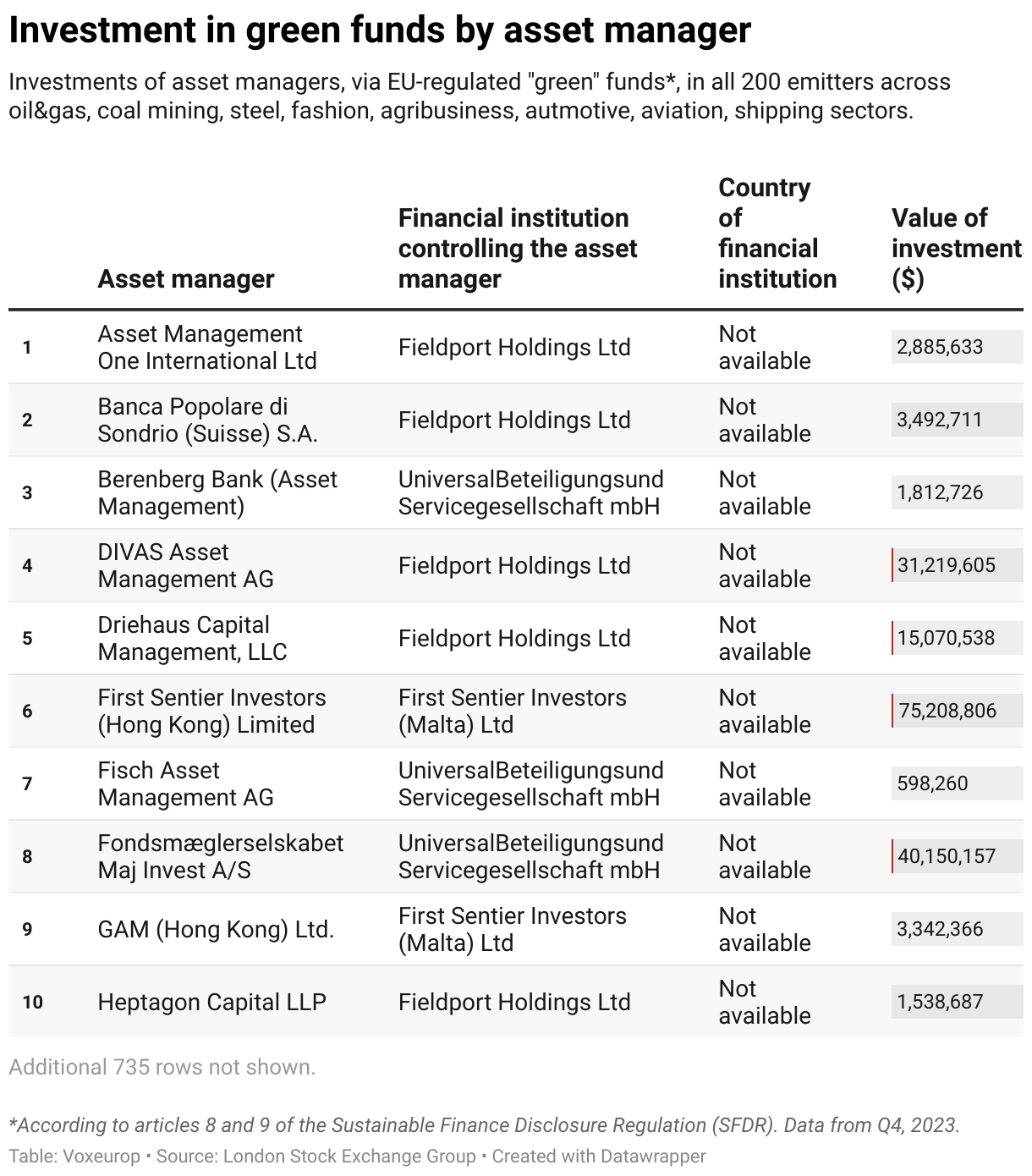

The top 10 “green” finance operators, by investment value, are Deutsche Bank Asset & Wealth Management (DWS), Black Rock Investment Management and Advisors Divisions, Credit Agricole Amundi Asset Management, Intesa Sanpaolo Eurizon Capital, Fidelity International, JP Morgan Asset Management, Northern Trust, Templeton, Allianz and Storebrand Kapitalforvaltning.

These financial institutions are members of the lobby group European Fund and Asset Management Association, which declined our request for comment.

Research from the last quarter of 2023, using data from the London Stock Exchange Group (LSEG), points to a system of weak regulation being exploited for profit, making it nearly impossible to limit global warming.

Climate disruption as investor profit

We found that the top 10 asset managers (named above) are responsible for more than a quarter of all investments by EU-regulated "green funds" – this is €87 billion – in the 25 biggest GHG emitters in each of the eight most carbon-intensive economic sectors – 200 companies in total (1). These sectors include fossil fuel extraction and refining (oil, gas and coal), agribusiness (deforestation, crop plantations, pasture, fertilisers, manure), transportation (road, aviation or shipping), steel production and fashion (2), and account for 60-70% of global carbon emissions, according to the International Panel on Climate Change (IPCC) and other sources (3).

Our analysis shows that these 200 top GHG emitters are, on average, responsible for 77% of the emissions of all listed companies in their respective sectors.

The 25 emitters in the oil, gas and coal mining industries released an average of 8.5 billion tonnes per year between 2017 and 2023 (almost three times the emissions of all 27 EU countries in 2022), accounting for 55% of the GHG emissions of all listed fossil energy companies on the planet.

Essentially, despite the colossal amount of carbon they emit, the 200 polluters we identified are still attracting billions of US dollars in supposedly responsible investments.

We found that 4,342 funds in Europe that invest in such companies are formally classified as 'green' because they are marketed under the EU's Sustainable Finance Disclosure Regulation (SFDR).

This regulatory framework, which came into force in 2021, requires asset managers to disclose the environmental and social objectives of the activities in which they invest investors' money, as well as the precautions taken to anticipate and minimise the negative impacts of such activities.

Our analysis shows that at least 738 financial institutions around the world (including those headquartered or with offices in the EU) have triggered investment flows into carbon-intensive companies marketed as SFDR-compliant.

Most of these institutions are based in France, Germany and Italy, as well as in the United Kingdom, the US and Hong Kong. Many of these funds are registered in tax havens like Luxembourg and Ireland, which host 61% of the EU's green financial market – that is $53 billion.

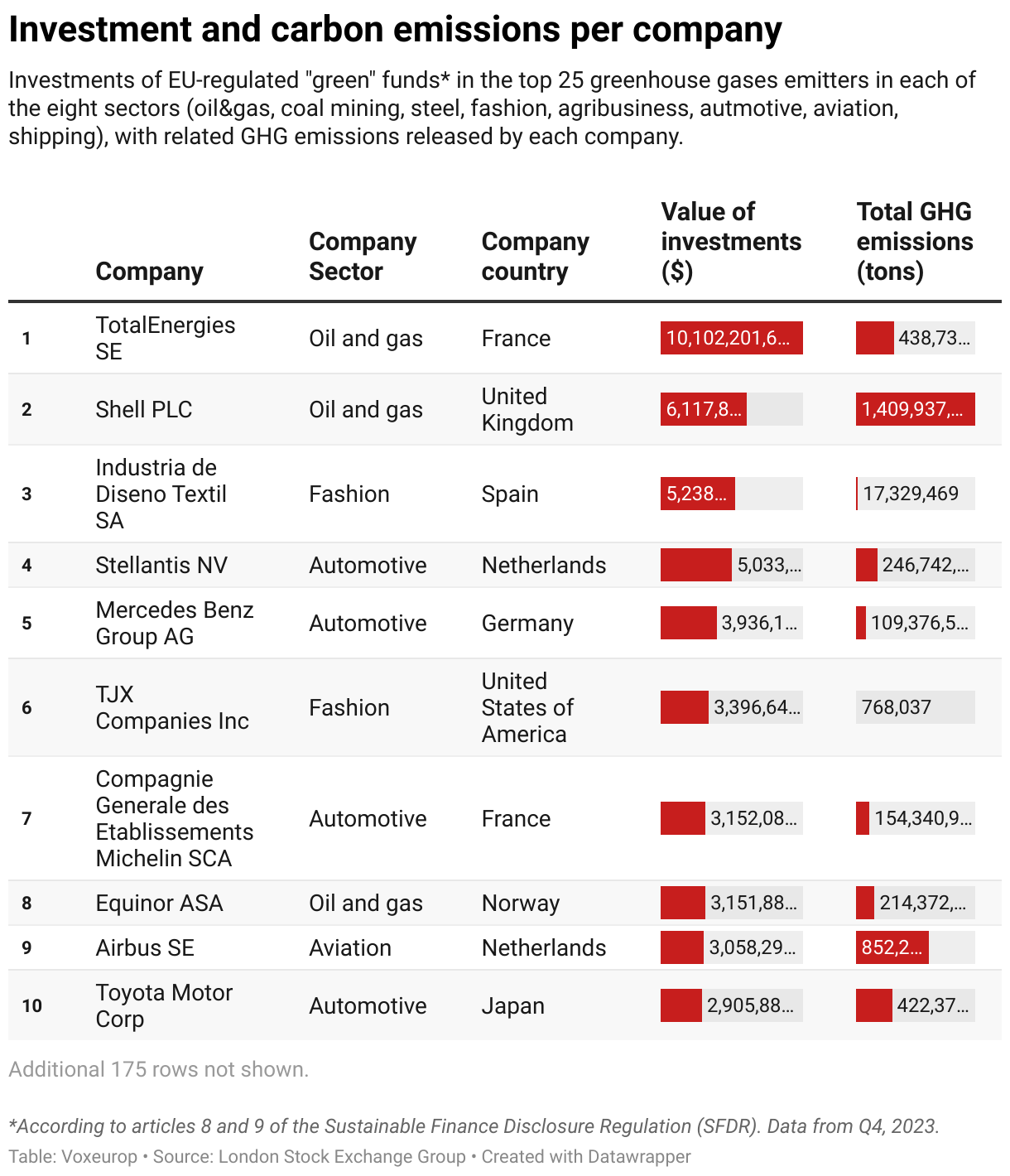

The oil and gas sector is the most popular among these self-labelled green funds, with $33 billion invested, followed by the automotive ($22 billion) and fashion ($15 billion) sectors. The three sectors equate to 77% of all supposedly "green" investments.

The top 10 carbon emitters across all sectors attracted more than half ($46 billion) of all the investments. They include the oil and gas companies TotalEnergies (France), Shell (UK) and Equinor (Norway); the car industry giants such as Stellantis (Netherlands), Mercedes Benz (Germany), Toyota Motor (Japan) and Michelin (France); the fashion brands Industria de Diseño Textil Inditex, owner of clothing retailer Zara (Spain) and TJX, one of the world's largest multinational off-price department store groups (US); and Airbus (France).

An EU-endorsed greenwashing?

Environmental activists say that this greenwashing hoax goes against the internationally binding 2015 Paris Agreement, when almost every country in the world committed to limit the rise in global average temperature well below 2°C compared to pre-industrial levels, and to even cap it to 1.5°C before the end of the century. The agreement calls for “finance flows consistent with a pathway towards low greenhouse gas emissions and climate-resilient development”.

As part of the European Commission's Green Deal, an ambitious plan to achieve climate neutrality in the EU by 2050, the SFDR framework was supposed to promote transparency about the carbon reduction (and other socio-environmental) benefits of financial products, in order to encourage investment in cleaner activities. However, loopholes and lax enforcement have allowed massive investment in carbon-intensive operations, as revealed in our September 2023 investigation and as confirmed by this fresh analysis.

We found that the top 25 largest emitters in all sectors accumulated $85 billion of investments from all funds that are supposed to “promote environmental and/or social characteristics” according to loose criteria arbitrarily chosen by each asset manager (Article 8 of the SFDR).

They also accumulated $2 billion from the few funds that declare themselves “100% sustainable” in accordance with their own – and often diverging – interpretation of the more stringent parameters set by the law (Article 9 of the SFDR).

Although the European Securities and Markets Authority (ESMA), which has an oversight mandate, reiterated in January this year that Article 9 funds can only make truly sustainable investments, the SFDR does not provide a clear definition of what constitutes a sustainable investment.

Nonetheless, since 2022, most asset managers have downgraded their funds from Article 9 to Article 8 in order to avoid higher compliance burdens and have more leverage to support large carbon emitters.“We want to support these sectors [...] and encourage companies to take measures to commit to transition pathways,” said a spokesperson at Allianz.

"Investing in high-carbon sectors does not conflict with the objectives of the SFDR, which relate to the transparency of sustainability investments, nor with the Paris Agreement, which promotes the transition to a low-carbon economy," added an Intesa Sanpaolo spokesperson.

It is worth noting that harmonised EU criteria for quantifying and disclosing carbon emissions and reduction targets, in line with the Paris Agreement objectives, will only come into force in 2025 under the new Corporate Sustainability Disclosure Directive (CSRD).

Meanwhile, the 10 green funds classified as Article 8 and 9, which invest the most in the largest greenhouse gas emitters, have secured shares worth a total of $9 billion and $800 million respectively.

Asset managers have often abused their disclosure obligations under the SFDR to create eye-catching labels for their funds, giving the impression that all the activities they sponsor are environmentally and socially responsible. This has been publicly acknowledged in a consultation launched by the European Commission on the implementation problems and options for an effective revision of the SFDR.

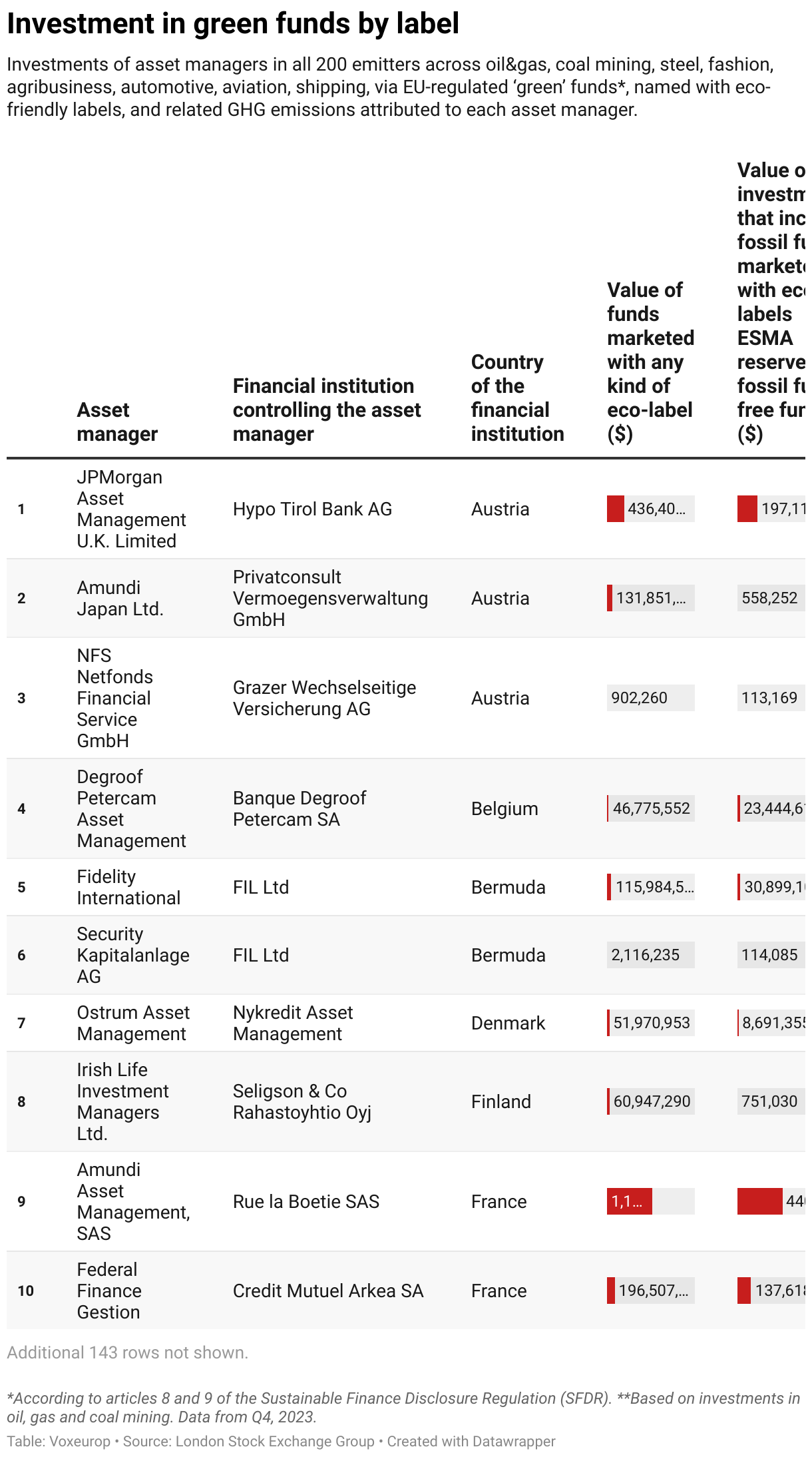

Over 20% ($18 billion) of the investments in top GHG emitters carry “green” names to attract investors (e.g. Blackrock's BGF Sustainable Energy Fund). This rises to 55% for Article 9 funds, with over $1 billion of eco-labelled shares in often questionable sustainable activities. In practice, asset managers use these green names (4) to promote their funds, even though they invest only a portion of the portfolio in environmentally and socially beneficial activities, reserving the rest for companies co-responsible for global warming.

For example, in its 2023 annual report, the world's largest bank, JP Morgan, admitted that its Europe Research Enhanced Index Equity (ESG) fund only sets "a minimum asset allocation of 51% in investments with positive environmental and/or social characteristics and a minimum of 10% in sustainable investments". JP Morgan declined to comment.

“Many of the funds are misleading. Investors cannot trust the claims made by these funds, so EU regulators need to step in and rectify this situation,” Lara Cuvelier, Sustainable Investments Campaigner at the NGO Reclaim Finance, told Voxeurop. “Guarantees must also be given to investors that such claims cannot be linked to investments that harm and threaten the European climate objectives.”

A long way to reform a flawed system

The SFDR is a mandatory disclosure framework and not a voluntary labelling regime, therefore [...] it should not be used for marketing purposes," said an ESMA spokesperson.

To improve transparency and fairness towards investors, the ESMA adopted an updated set of guidelines on the use of eco-related terms in fund names in May 2024.

Only funds that comply with the EU's Paris-Aligned benchmark, and therefore do not invest significantly in oil, gas and coal, are allowed to use the terms "ESG", "green", "climate", "environment", "sustainability" or "impact" in their names (this safeguard is in place because fossil fuels contribute to maintaining high emissions in the other sectors that burn fuel for their operations).

The same types of labels are also allowed to promote funds that enable a low-carbon pathway for fossil energy companies, provided they meet the EU Climate Transition Benchmark (which sets milder conditions).

However, ESMA's recommendations will not come into force until autumn this year (due to lengthy bureaucratic procedures) and are not legally binding. It is up to national regulators to decide whether or not to enforce them in their respective markets.

So far, misconduct in green finance has gone largely unpunished in EU member states, unlike in the US, where Deutsche Bank's asset management arm DWS was fined $25 million by the Securities and Exchange Commission – the US financial watchdog – in 2023.

In its report on greenwashing, published at the beginning of June 2024, ESMA said that competent authorities "face challenges in identifying breaches where the regulatory framework is based on unclear or ambiguous definitions" and that none of them "have submitted cases to law enforcement authorities".

We found that 7.5% (457) of Article 8 and 9 funds are incorrectly labelled as green according to ESMA guidelines. These funds have invested almost $6.5 billion in shares of the largest greenhouse gas emitters in the oil, gas and coal industries. This includes over $19.5 million in funds claiming to be "fully sustainable". These investments represent nearly 20% of all SFDR "green" investments in the 25 largest hydrocarbon companies we analysed.

Only 45 funds, mostly classified as Article 8, currently declare themselves to be aligned with the Paris Agreement, representing less than 0.5% of all SFDR investments in our 200 companies. Despite avoiding fossil fuels, these ESMA-compliant funds still invest $148 million in the top 25 emitters in other sectors, most notably transport, agribusiness, and fashion.

"Almost all the companies we rate do not respect the objectives of the Paris Agreement," said Axel Pierron, associate director of the Morningstar/Sustainalytics rating agency, whose analysis on 10 June revealed that 1,600 funds will have to change their names or divest around $40 billion if they want to comply with ESMA's crackdown on greenwashing.

"We comply with all the regulations in force for investment funds, including those for sustainable or ESG funds, and if they change, we [...] ensure compliance [...]," said an Amundi spokesman.

The same message was echoed by some of the other top 10 financial players. "Regarding the labelling of our funds, we are [...] reviewing both existing and future names as new regulatory baselines emerge," said the Allianz spokesperson. A DWS spokesperson confirmed that an "analysis of their products had started "based on ESMA's final report”. A JP Morgan spokesperson confirmed the company was "currently reviewing the final ESMA guidelines". Finally, a BlackRock spokesperson said the company would "adapt to any relevant changes in the evolving policy landscape".

Financial institutions have somewhat resisted ESMA's attempt to clean up the green finance markets. They did not accept that fund portfolios should contain a minimum of 50% sustainable investments as a condition for "sustainability" labelling. Nor have they accepted the introduction of thresholds to limit the negative impacts of the activities supported by their funds.

Not to mention the criticism of the Paris approach that was eventually adopted by ESMA. During the working meetings of the UN-convened Net Zero Alliance initiative, which brings together leading financial players, it was argued that overly ambitious decarbonisation targets "foster divestment".

"We recognise that climate change is one of the most pressing threats facing our planet [...]," said a spokesperson for Fidelity International, a member of the Net Zero Alliance, "We believe that driving change through a positive engagement approach, rather than a policy of exclusion (or disinvestment), is the most effective way to positively influence corporate behaviour."

Asset managers have also won the right to use the "transition" label for funds investing in fossil fuels, with no decarbonisation requirements until 2025. Only then will companies in their funds have to publish their climate transition plans under the new Corporate Sustainability Disclosure Directive.

At present, most of the 'transition' labelled funds (which still represent a relatively small proportion of total investments) do not have decarbonisation target tracking indicators.

The "Portfolio Climate Transition Share" fund marketed by the French pioneer of sustainable investing, Carmignac (which, like its larger rivals, is active throughout Europe), includes three carbon powerhouses. These are the French oil giant Total Energies, the Swiss coal miner Glencore and the German utility RWE.

According to a Carmignac spokesman, all three of them are among the "companies offering low-carbon solutions" and "enabling others to reduce emissions" in which the fund has decided to invest. However, no information is given on the targets and timetable for the announced GHG reductions.

"I would not exclude big polluters from green funds which, through such investments, should be encouraged to reduce their emissions,” Richard Heede, co-founder and director of the Climate Accountability Institute, told Voxeurop. “But investments that do not hold companies to their climate commitments are not helpful."

The implementation of the new Corporate Sustainability Disclosure Directive next year may bring some improvements. According to Pierre Garrault, Senior Policy Adviser at the European Sustainable Investment Forum, the dedicated EU standards will “offer more incentives for companies to reduce their carbon emissions, and disclose comparable data for investors to make informed investment decisions.”

"To combat greenwashing, it's essential to align green finance laws such as the Corporate Sustainability Disclosure Directive and those under review, and ensure financial institutions provide accurate information to investors," said Mathilde Nonnon, Sustainable Finance Policy Officer at WWF in Brussels. "We also need a clear, strict categorisation of funds with minimum criteria to ensure that investments are truly aligned with stakeholders' desire to invest sustainably."

Mid-June 2024, ESMA, along with the EU banking and insurance market authorities (EBA and EIOPA), proposed reforms to the Sustainable Finance Disclosure Regulation. They suggested introducing two voluntary product categories, "sustainable" and "transition," with clear objectives and criteria to reduce greenwashing. They also proposed a sustainability indicator to rate financial products.

The carbon footprint of green funds

The European Union has set benchmarks that allow asset managers to evaluate the climate performance of their investment funds based on "carbon intensity". This means they look at how much carbon companies in their portfolio emit for every euro they produce, compared to others in the same industry (e.g., Shell in the oil and gas sector).

However, these rules can have unintended negative consequences. If companies in a fund make more profit per tonne of CO2, or increase their carbon emissions less than the sector average, the fund can still claim improved climate benefits and earn green labels, even if its total emissions have increased.

Carbon intensity performance is usually determined by company assessments or market indices created by rating agencies using their own arbitrary criteria. These criteria are expected to become more independent and transparent under upcoming EU requirements. This makes it easy for asset managers to create a high-performing portfolio by excluding only the red-flagged emitters or by selecting favourable indices.

For example, HSBC, Europe's largest bank by assets, offers a fund called Developed World Sustainable Equity. This fund's companies have a total carbon intensity that is 50% lower than the market index, as determined by the rating agency FTSE Russell. However, when the market index performed poorly in 2023 compared to 2022, the fund's climate performance also dropped accordingly.

"Current metrics show that this exchange-traded fund is meeting its objectives while closely tracking its parent index," said a spokesman for HSBC, which is retaining its eco-label only because the sectors of the companies it invests in have performed worse overall than its own fund.

Experts say that the carbon-intensity approach can help set more realistic targets by considering company growth and ensuring fair treatment across different sectors. However, this approach allows emissions to increase as companies expand, though at a slower rate than if no measures were taken.

However, science-based models show that the Paris Agreement trajectory requires a linear net reduction in absolute carbon volumes. "Relying only on reducing carbon intensity is not enough in the long term, as we could risk exceeding the global carbon budget, above which temperatures would rise beyond dangerous levels," explained Diana Urge-Vorsatz, IPCC vice-chair.

There's an ongoing debate in the financial sector about whether asset managers should focus on measuring the greenhouse gas emissions financed by their funds, as required by the SFDR, rather than just looking at carbon intensity. This approach could provide a better understanding of the climate impact of their investments.

Fabio Moliterni, climate finance expert at Etica Sgr, explains: "By supporting carbon-emitting activities, asset managers indirectly cause significant negative impacts. There's potential in holding them accountable for some of the emissions generated by the companies in which they invest".

For example, since EU-regulated funds hold on average 0.5% of the traded shares of the top 25 emitters in oil, gas and coal production, they are effectively responsible for 0.5% (around 115 million tonnes) of these companies' annual carbon emissions (5). Of these emissions, around 33% (39 million tonnes) are attributable to the top 10 asset managers, while 18% (20.5 million tonnes) are linked to the top 10 “green” funds.

"This is always an 'accounting' exercise with its flaws," notes Moliterni, "but it's an important way of highlighting and comparing the true climate impact of the financial sector.’

Luca Poggi, data analyst at Transport & Environment, emphasises the importance of looking at all emissions, both direct and indirect. “This allows investors to know exactly how much carbon they are financing with their money.” he said, while “companies cannot hide bad environmental behaviour behind low direct emissions and are encouraged to take their entire value chain into account.”

This makes stricter rules all the more urgent: a recent academic study found that almost a quarter of the green funds analysed had higher CO2 emissions than their benchmarks when all indirect emissions were taken into account. Things may be looking up, however: from 2025, new European sustainability reporting standards will require companies to disclose their indirect emissions when reporting their carbon footprint. Fingers crossed they will comply.

Footnotes and methodology

- We selected the 25 largest greenhouse gas (GHG) emitters in each of these 8 sectors: oil & gas, coal mining, steel, fashion, agribusiness, automotive, aviation, shipping, To identify such companies we used both direct GHG emissions (Scope 1) generated by the company's operations and indirect GHG emissions generated by both the company's energy consumption (Scope 2) and the activities of the company's suppliers and the use of its products and services by customers (Scope 3). Emission volumes are based on company reports or estimates made by LSEG Data & Analytics. We chose to include Scope 3 because the EU believes that companies must also address these indirect emissions in order to meet the targets of the Paris Agreement. We analysed the composition of the funds formally complying with articles 8 or 9 of the SFDR and we selected those including, in their portfolio, the top 25 GHG emitters in each of the 8 critical sectors. Our analysis is a snapshot of the funds as recorded by the end of the third quarter of 2023, so their composition may have changed since then, depending on sales and purchases. We found that of the 200 companies we selected across the 8 sectors, 14 companies operating in the oil, gas, coal, agribusiness, shipping and steel sectors are not included in the portfolio of the Article 8 and 9 funds. Indeed, the funds investing in these companies have clearly declared themselves as not 'green' (according to Article 6 of the SFDR). However, these 14 companies represent less than 4% ($190 million) of all SFDR investments in the 200 companies and account on average for slightly more than 1 of the weighted GHG emissions (11 million (scope 1,2,3)) of all 25 companies in their respective sectors. Their quantitative impact on the results of our analysis is therefore negligible.

- Our analysis does not include data from energy production based on fossil fuels, the most carbon intensive sector, which you can read about in a forthcoming article.

- Fashion and steel respectively account for 8-10% and 7-9% of global carbon emissions.

- The first group includes terms that, according to ESMA guidelines, should only be used by funds that do not invest in fossil fuels, such as "ESG", "green", "climate", "environmental", "impact", "sustainable" (including the acronym "SRI" - Sustainability Related Index). The second group includes all other eco-related terms such as "clean", "responsible", "renewable", "net zero", "transition". The third group includes the acronyms of the two EU benchmarks CTB (Climate Transition Benchmark) and PAB (Paris-Aligned Benchmark), which is often referred to by its synonym “Paris-aligned”. In addition to the terms we have identified, many others may be included in the names of all 4,033 and 309 funds classified under Article 8 and Article 9 of the SFDR, respectively, that we have analysed.

- We used company greenhouse gas reports and estimates from LSEG Data & Analytics and applied a simplified version of the Financed Emissions Standard set by the private sector platform Partnership for Carbon Accounting Financials, assuming that each share represents a fraction of the company's total emissions. The greater the number of shares held in a company, the greater the volume of carbon emissions for which a fund and the asset manager marketing it are responsible. We could not quantify and attribute to asset managers the total emissions of all 200 emitters in all sectors because of the frequent overlap between direct and indirect emissions and the risk of double-counting and over-estimation. Indeed, the direct emissions of oil, gas and coal companies (Scope 1) are also reported as indirect emissions (Scope 2) by companies in other sectors that purchase and burn fossil fuels for their operations and therefore need to account for the emissions caused by their energy suppliers. For example, direct emissions from oil and gas fields and refineries reported by Shell are also reported as indirect emissions by Airbus, which manufactures aircraft using energy supplied by Shell, and by Air France, which flies Airbus aircraft using fuel also supplied by Shell.

Stefano Valentino is a Bertha Challenge Fellow 2024.

This article is part of the investigation coordinated by Voxeurop and European Investigative Collaborations with the support of the Bertha Challenge fellowship. With the contribution of Alef Ferreira Lopez, Data Analysis Assistant, PhD Scholar in Economics, Universidade Federal de Minas Gerais

Do you like our work?

Help multilingual European journalism to thrive, without ads or paywalls. Your one-off or regular support will keep our newsroom independent. Thank you!