Select a language

Chapter 3

Behind the green curtain, biodiversity is being destroyed

In the previous chapters, we saw how in 2018 Michelin used green bonds to finance the rubber plantations of its new Indonesian partner Royal Lestari Utama (RLU) in the Indonesian province of Jambi, on the island of Sumatra. The bonds, designed to support sustainable projects and marketed by BNP Paribas, were issued by the new sustainable-finance platform Tropical Landscapes Finance Facility (TLFF). They were also endorsed by a number of third parties who were found to have based their assessments solely on documents.

Michelin and its partners also ignored warnings from grassroots organisations about the industrial-scale deforestation previously carried out by RLU's local subsidiary.

👉 Read chapter 1: European green finance is paying for deforestation in Indonesia: the case of Michelin

👉 Read chapter 2: How a project decried for its environmental impact became a flagship of European green finance

In order not to jeopardise the success of a model project, Michelin and the founders of the TLFF failed to communicate these facts to potential investors, who might have been less enthusiastic if they had known about them. We will now look at how all this was possible – and why it should not have been, given the rules of green finance and the situation on the ground in Sumatra.

It was the "visa" granted in January 2018 by the ethical-investment ratings agency Vigeo Eiris, certifying compliance with the principles of the International Capital Market Association (ICMA), that allowed TLFF bonds to be registered in the database of Climate Bonds Initiative. CBI is the world's leading certifier of climate fundraising, and Vigeo Eiris is a CBI-approved auditor.

The accreditation of the bonds in the CBI's Climate Friendly Investment Showcase helped their reputation and visibility to potential investors. "Our database is searched to see what is green. If bonds do not meet the criteria of our database, they cannot be included in the green-bond indexes," explained Caroline Harrison, research director at CBI, to Voxeurop. This was confirmed by Alex Wijeratna of the environmental NGO Mighty Earth: "Portfolio managers can assume that if TLFF bonds are part of a reputable green index, then the investment is good to go."

CBI considered that Royal Lestari Utama's plantations provided benefits for climate protection, since the cultivation of rubber trees was a form of carbon sequestration. Furthermore, the involvement of local farmers in rubber production, alongside food crops, improves their living conditions and prevents them from having to further expand their agricultural land at the expense of forest areas.

Relying on the flawed Vigeo Eiris assessment (see Chapter 2), CBI endorsed the TLFF's obligations without taking into account the greenhouse gases released by past deforestation. CBI could not have been aware of this, given that RLU and BNP had failed to report it to Vigeo Eiris. Moreover, CBI’s methodology in the agricultural sector considered that a reduction in emissions during the period of the investment - which in this case officially began in 2018 (the date of the transaction by TLFF) - was sufficient. However, we learned (see Chapter 1) that the green bonds were partly used to finance, retroactively, the clearcutting that took place prior to the joint venture between Michelin and Barito. Rather than sequestering carbon, this deforestation contributed to carbon emissions.

A breach of the principles of green bonds

In a letter to the Climate Bonds Initiative in March 2021, Mighty Earth asked it to remove the TLFF bonds from its database. The environmental NGO argued that "this failure to disclose [...] the known key information that the subsidiary of Michelin's local partner [...] was one of the major causes of the land clearing and deforestation on its concessions in Jambi [...] constitutes an extremely serious - and ultimately misleading - omission and [...] a gross violation of Green and Sustainability Bond principles" established by ICMA. These require transparent disclosure of the environmental risks associated with funded projects (1).

According to an ICMA expert on sustainable finance who wished to remain anonymous, "it should be clear that land conversion and deforestation are not in the spirit of green bonds, even assuming that the final [outcome] is green, as in the case of sustainable agriculture for example. External auditors and investors would doubtless not endorse this [as] their reputation could suffer." Indeed, ICMA principles require that the sums collected through green bonds be invested, among other things, in the “environmentally sustainable management of living natural resources and land use (including environmentally sustainable agriculture; [...] environmentally sustainable forestry, [...] and preservation or restoration of natural landscapes).

As unveiled by Voxeurop through analysing official documents (see Chapter 1), RLU used a third of the borrowed money to repay previous bank loans, with which it financed land clearing and rubber plantations developed before Michelin joined the game. These activities certainly do not represent an example of "sustainable management" as defined by ICMA.

On the subject of Mighty Earth's initiative, Sean Kidney, executiver director of CBI, told Voxeurop: "We don't do field checks, we rely on independent reviewers. In this case, the bonds had received a second opinion [the assessment of Vigeo Eiris, a ratings agency specialised in ethical investments] and the original documents made no reference to any deforestation. On the other hand, if we find out from our own sources in Indonesia that there has been a problem, then we will simply remove the bonds from our list. Indeed, under our retrospective period, no deforestation must have taken place in the last ten years." Michelin has already repaid the bonds to investors, so any action by CBI would now come a little late.

Paul Vermaak, director of standards at CBI, told Voxeurop: "Our database can accept bonds that support the sustainable transition of agribusinesses with a history of land conversion – i.e. it must have taken place long before – but not those that might support companies that have cleared the forest just before publishing a 'no-deforestation policy'. This would be a manipulation of the system to unfairly extract money from investors. It would be up to ICMA's qualified reviewers to avoid such an unintended consequence."

Vermaak confirmed that "if the company has deforested the land, this means that it has generated significant [carbon] emissions and removed a high-carbon-sequestration habitat, before replacing it with lower-sequestration agricultural production activities. Such a scenario is implicitly inconsistent with our taxonomy" (2). He added that the CBI is committed to revising its assessment criteria to exclude, in the future, any project that does not comply with the "Do no significant harm" (DNSH) principle (3).

To hide the clearcutting that preceded the joint venture between Michelin and Barito Pacific could thus reasonably be described as a breach of the green-bond guidelines set out by the International Capital Market Association and the CBI. It also compromised RLU's adherence to the Environmental and Social Sustainability Performance Standards of the International Finance Corporation (IFC), the private investment arm of the World Bank.

Indeed, the environmental, social and governance (ESG) criteria mentioned in the green-bond prospectus proclaim full compliance with the ICMA principles as well as with the IFC standards. Royal Lestari Utama should therefore have been subject to the same environmental and social requirements as those for companies applying for IFC funding. In its Second Party Opinion – a form of audit – Vigeo Eiris made it clear that the environmental benefits of the project "are conditional on the implementation of the [...] IFC performance standards".

Among these, the chapter on conservation blacklists projects that result in a net loss of biodiversity – a concept that includes any natural forest that represents an important habitat for threatened species or for indigenous communities.

Without referring specifically to RLU, the IFC press office suggested that its venture might well fall under this non-compliance clause. In an email exchange with Voxeurop, it said that "the implementation of the national legal framework" and "the company's non-deforestation policy do not come into play [...], i.e. it does not matter whether or not the company had such a policy or a clearing permit (where it has degraded the habitat), it still has to prove [...] that its project resulted in no net loss (of biodiversity) [...]" to comply with the IFC standards.

In particular, the IFC considers that companies are liable for any biodiversity loss they cause by deliberately degrading a natural habitat "in anticipation of obtaining financing from a lender [...] for the project".

Deforesting and replanting, as quickly as possible

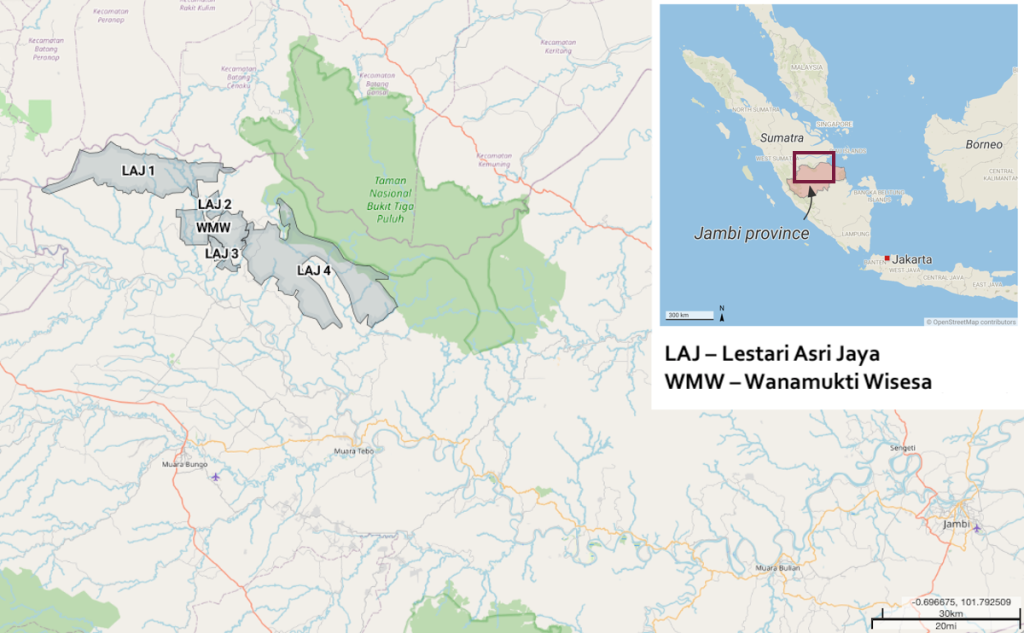

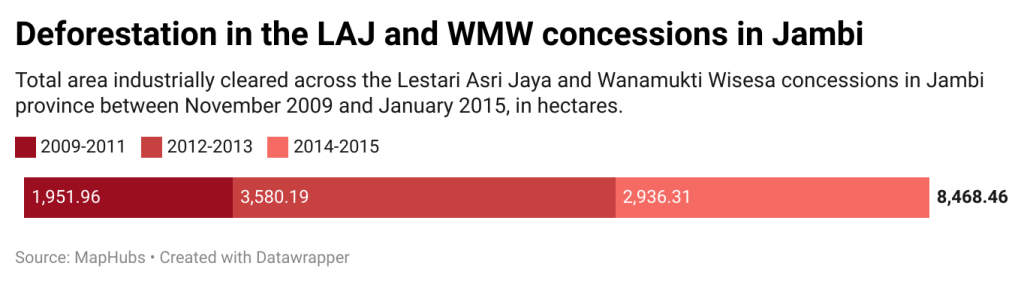

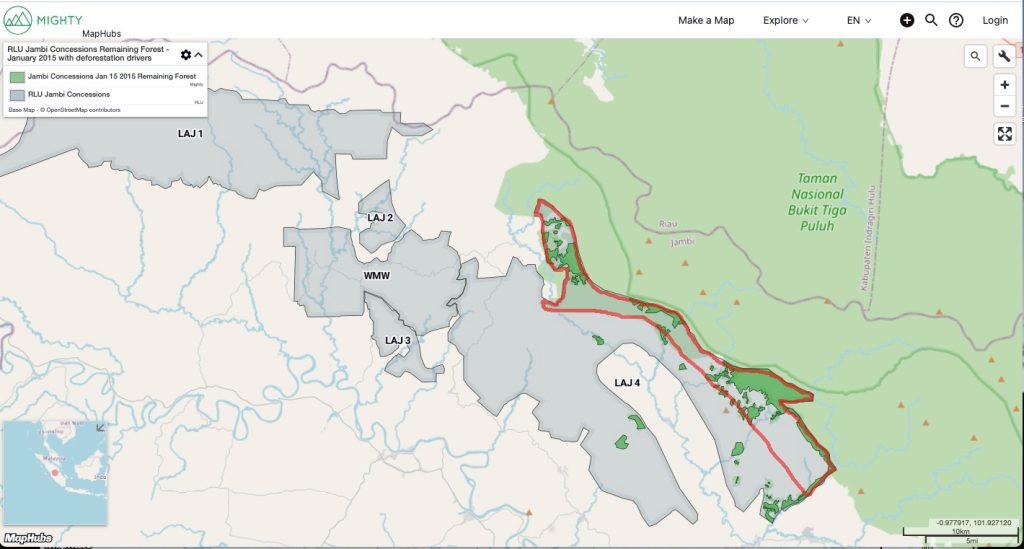

This seems to be exactly what happened. The confidential report of the auditing firm TFT/Earthworm, seen by Voxeurop, shows that Lestari Asri Jaya (LAJ), the RLU subsidiary that operates the Jambi concessions, continued to clear land until late 2014. Indeed, according to both the green-bond prospectus and the latest independent report on environmental protection in the LAJ concession, published in May 2022 by Remark Asia and Daemeter Consulting, rubber planting in fact exploded (4) between early 2013 – when Michelin first visited the site – and late 2014, when the joint venture was signed.

"The Michelin-Barito Pacific joint venture had planned from the start to seek new financing," a source familiar with the RLU project told Voxeurop on condition of anonymity. "But the banks did not consider the rubber plantations to be assets sufficient to constitute a mortgage guarantee, as the joint venture had hoped. And that was because the land is owned by the government, and the government's licence to RLU is time-limited."

According to Alex Wijeratna of Mighty Earth, "All of this is evidence enough that the conversion of the forest to rubber plantations was accelerating in anticipation of the deal that Michelin and Barito Pacific had been negotiating for months. It seems that their intention was precisely to maximise the plantation area in order to secure financing for their project, which in reality had begun long before the joint venture and RLU's declaration of non-deforestation."

The prospectus of the green-bond offering marketed by BNP Paribas confirms that total production includes rubber trees planted before 2015. These account for more than half of the area converted at the time of the bond issue.

Wijeratna concludes: "It is reasonable to say that these green bonds are the result of a long-planned quest for funding. Habitat destruction is being pushed forward with the complicity of Michelin." (Map 1)

The decision to clear the forest to plant rubber trees does not even appear to qualify under an IFC derogation, which states that "significant degradation of the natural habitat will only occur if" the company in question "can demonstrate that no viable alternative exists for the project". The report on LAJ by Remark Asia and Daemeter Consulting states that in 2010 there were over 17,000 hectares of open space and bushland (27% of the concession) available for rubber planting.

"It is reasonable to say that these green bonds are the result of a long-planned quest for funding. Habitat destruction is being pushed forward with the complicity of Michelin."

Alex Wijeratna, Campaign Director at the NGO Mighty Earth

"From 2014, during our successive field visits, we observed areas that had been deforested and planted with rubber trees, even though they were unsuitable for rubber farming. Conversely, other areas, more suitable, were not being exploited," confirmed Hervé Deguine, Michelin's public affairs director, to Voxeurop. "There was a government plan that RLU was supposed to follow regardless of the situation on the ground, by which it should avoid continuing to plant in places that were not suitable from an agricultural point of view. But [in practice] it often contested this", he added.

All this is to say that the Royal Lestari Utama project does not strictly comply with International Financial Corporation standards. These standards would hold the company responsible for the loss of biodiversity that it caused – before adopting its no deforestation policy for the joint venture – by its clearing of the forest in spite of the available alternatives.

”Natural" deforestation: a convenient option for Michelin and its partner

In a response published a few weeks after a Mighty Earth report revealed the extent of deforestation carried out by its subsidiary Lestari Asri Jaya in its Jambi concession, RLU explained that industrial deforestation prior to the signing of the joint venture was only in areas "already considered degraded, logged or shrub land at the time these licences were initially granted".

Deguine confirmed to Voxeurop that Michelin still supports the position that RLU expressed before it was bought out by the French multinational. "Whether Michelin is a minority shareholder, as it was in the past, or a sole shareholder, as it is now, does not change anything in this respect," he told Voxeurop.

Johan Kieft, secretary-general of the TLFF financing platform and UNEP’s green-economy expert, also agrees with Royal Lestari: "RLU has only cleared areas that have been identified as having low biodiversity or low carbon [storage] value based on independent verification and monitoring." Kieft sent us a presentation which does not, however, confirm his claim.

Such statements may give the false impression that before RLU's intervention, the habitat was already so degraded that clearcutting did not result in substantial biodiversity loss.

This is exactly how the Climate Bond Initiative saw the case: "Following Mighty Earth's complaint, we made inquiries and it appears that the small piece of land in question was degraded land that had been turned into a rubber plantation," said Sean Kidney, CBI's executive director, to Voxeurop.

However, the International Finance Corporation is clear that "human-induced habitat modification is [...] not necessarily an indicator of its biodiversity value" and "if, in the opinion of a competent professional, the habitat still contains [...] one or more native ecosystems, it should be considered a natural habitat, regardless of its degree of degradation."

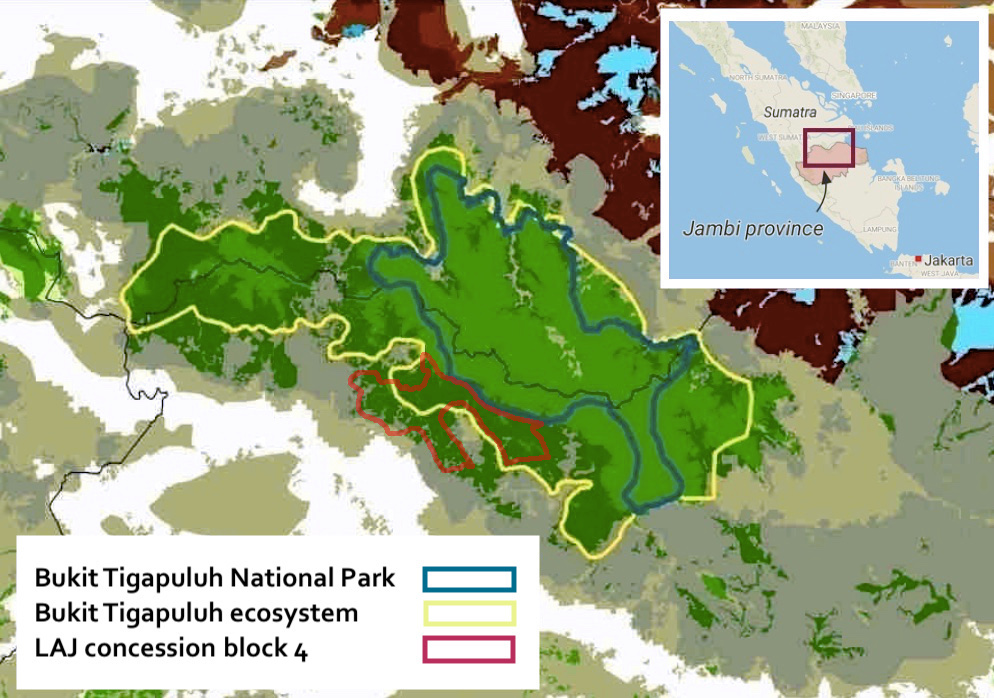

Indeed, environmental experts and documents consulted by Voxeurop confirmed that the area cleared by RLU’s subsidiary Lestari Asri Jaya was still an integral part of the forest habitat of the Bukit Tigapuluh National Park and its surroundings, which the Indonesian government itself had deemed vital for endangered species (map 1) (see chapter 4).

Royal Lestari Utama thus seems to have damaged an ecosystem which, although already degraded, was still a forest and a natural habitat. It did not adhere to the green-bond standards of the International Capital Market Association and the Climate Bonds Initiative. And it did not meet the environmental performance standards of the International Finance Corporation. It failed in its obligation to its investors.

End of chapter 3

In the next chapter of our investigation, we will look at how Royal Lestari Utama managed to obtain timber permits from the deforestation of areas with endangered ecosystems in order to plant them with rubber trees partly financed with green bonds obtained by its partner Michelin.

Notes

1) These principles "emphasise the need for transparency, accuracy and integrity of information disseminated and included in issuers' reporting to stakeholders". They state that "the issuer of a Green Bond is strongly encouraged to disclose to investors [...] additional information about the processes by which the issuer identifies and manages the social and environmental risks associated with the project(s) concerned".

2) The Climate Bond Taxonomy "identifies the assets and projects needed to achieve a low-carbon economy and provides criteria for screening GHG emissions consistent with the 2-degree global warming target set by the 2021 Paris Agreement."

3) This was introduced into the European Union's environmental taxonomy to ensure more effective protection of biodiversity as part of the Post-Covid Resilience Plan.

4) From 882 hectares converted to rubber plantations at the end of 2012 to 5782 hectares at the end of 2014.

👉 Glossary and abbreviations

👉 Read chapter 1: European green finance is paying for deforestation in Indonesia: the case of Michelin

👉 Read chapter 2: How a project decried for its environmental impact became a flagship of European green finance

Field work in Indonesia conducted by our media partner Tempo was supported by a grant from the Global Initiative Against Transnational Organized Crime. The investigation was also supported by the Environmental Reporting Collective, Journalismfund.eu and Mediabridge.

With the support of Investigative Journalism for Europe

Was this article useful? If so we are delighted!

It is freely available because we believe that the right to free and independent information is essential for democracy. But this right is not guaranteed forever, and independence comes at a cost. We need your support in order to continue publishing independent, multilingual news for all Europeans.

Discover our subscription offers and their exclusive benefits and become a member of our community now!