Select a language

On Prague's Pařížská Street – one of the most expensive in Central Europe – is a discreet dark brown door. Behind it is the headquarters of the Energetický a Průmyslový Holding – or EPH, a holding company. This is Czechia's largest company, whose dividends to its shareholders in 2021 amounted to almost €850 million. It is owned by businessman Daniel Křetínský, whose personal fortune approaches 120 billion Czech crowns (CZK), almost €5 billion.

Daniel Křetínský is a Czech lawyer whose career began at the Slovakian financial group J&T. A jack-of-all-trades, he has investments in energy across Europe, in the French media (including the newspaper Le Monde), in the investment fund Vesa, in the British Royal Mail and the Dutch postal service PostNL. In September 2022, Křetínský – the fourth richest Czech citizen – bought a luxury mansion near Paris for tens of millions of euros, which he plans to convert into a hotel. He also owns the Sparta Prague football club and a stake in London's West Ham United.

In the first half of this year, EPH posted a profit of nearly €1.3 billion – slightly more than in the whole of 2021. The reason is obvious. Even more than last year, EPH is benefiting from rising prices for electricity and gas. The current crisis precipitated by the Ukraine war is a contributing factor.

A good crisis

Paradoxically, today's energy crisis is saving Křetínský's company. EPH Holding's growth in 2021 was due entirely to the rise in energy prices.

Until now EPH has focused on the transport of Russian gas to Europe, but this remains a shaky business. As the company recently admitted, changes to long-term contracts or to regulated tariffs could have a “significant negative effect on the group's business”.

Křetínský has plenty to worry about. EPH's historical growth was due entirely to its stake in the Slovak company Eustream, the largest Russian gas transporter to Europe. The investment was made in 2013 for an estimated €2.5 billion. It was a juicy deal: his holding company grew from CZK 81 billion to CZK 340 billion (about €14 billion) in assets, its revenues more than doubled in a year, and it ended up as one of the three largest Czech companies. This meant enough cash to expand rapidly in the gas sector and, above all, to pay back billionaire Peter Kellner's financial group PPF, which had invested in EPH when it was founded (Kellner meanwhile died in a helicopter crash in Alaska in 2021).

How Křetínský bagged the golden goose

Buying the Slovak gas power plants would not have been possible without the blessing of the authorities in Bratislava. At the time, the government was led by the social democrat Robert Fico. This was the first time – but not the last – that the Fico government would help EPH to buy Slovak energy companies.

In 2012, for example, EPH bought a 49% stake in Slovenský Plynárenský Průmysl (SPP) from its French and German owners, GDF Suez and E.ON. SPP manages, among other things, the Eustream gas pipeline, which runs through Slovakia and is one of the main gateways for Russian gas to the European Union. The deal was made with the consent of the Slovak government, in a transaction valued at €2.6 billion. The Slovak state retains a 51% stake in SPP, but EPH exerts the managerial control.

The sale was preceded by a deal with the Fico government, under which EPH would hand over its loss-making domestic gas supply division to the state in exchange for the government maintaining its protection of EPH’s “golden goose”: the transit of Russian gas through Slovakia, provided by Eustream. SPP has a long-term gas supply contract with Russia's giant Gazprom that expires in 2028.

As part of the deal, shareholders would have shared an annual dividend of at least €600 million per year for five years. To buy the shares, EPH secured a €1.5-billion loan from an international consortium of banks. It then raised the funds needed to repay the loan by means of pre-agreed dividends and a reduction in the share capital of over €1.2 billion.

Through a structure based in the Netherlands, GDF Suez and E.ON had for their part saddled Eustream with debt, through a bond issue worth almost €1.25 billion. EPH therefore de-facto financed the entire purchase with funds it had itself taken from the company it was buying.

Robbing Peter to pay Paul – it is a strategy that Křetínský seems to know well. In 2015, EPH had raised more than €750 million in loans from Slovak gas companies through its subsidiaries. Again, it did not have to pay them back out of its own money: they were simply rolled into future dividends. In three years, more than €1.75 billion was taken from Slovak gas power plants for EPH's investments and to pay off its other shareholder, PPF. In finance, money cannot be left to sleep. One must invest it, whether or not one has it.

Investing at all costs

Although EPH slightly reduced its loans and credits between 2016 and 2020, this situation did not last. The group's debt increased by almost €1 billion from 2020 to 2021. And according to results for the first half of 2022, the volume of long-term loans and credits continues to grow.

EPH paid record dividends in 2020 while reporting higher debt the following year. At the end of 2020, profits from gas transmission operations accounted for 38.8% of total group profits, but only 23.3% a year later. According to EPH's annual report, profits from gas transport had fallen by 53% in one year. And the war in Ukraine had not even started yet.

With one hand, Křetínský makes his investments outside the energy sector with funds from EPH. With the other, he drives his company into debt. Meanwhile, his personal fortune keeps on growing: from CZK 8 billion in 2013 to CZK 119 billion now – about €4.8 billion. An increase of more than a third compared to last year.

Investments have continued in 2022 – and not just in French real estate. Since the start of the war in Ukraine, Křetínský has announced plans to increase his stake in the Casino Group and the Fnac-Darty retail chains, two French companies where he is involved alongside the Slovak investor Patrik Tkáč.

A risky business

The entire EPH group is now de-facto based on two pillars: EP Infrastructure, which transports, stores and distributes gas; and EP Power Europe, which focuses on power generation.

The group's net debt is €4.5 billion. Of this, fully €2.9 billion belongs to EP Infrastructure, which appears to be highly leveraged and therefore risky.

This is also evident from the loans and bonds with which EPH has financed its acquisitions in the past. Most of these are on the books of EP Infrastructure. And it is this branch of the holding company that is now threatened by the decline in Russian gas supplies: the lower the quantity of gas transported, the less profit EP Infrastructure makes and the less able it is to repay its debts to banks and investors.

The group acknowledges this threat in the prospectuses of the bonds it issues: "It is possible that the EPH group may face a liquidity shortage that could ultimately affect its ability to repay its debts," reads the document published this summer.

New debts for Slovakian power plants

The situation of the highly indebted Slovenské Elektrárne, which produces almost 60% of Slovakia's electricity (almost half of which is nuclear), could also affect the overall health of the group. On 28 July 2016, EPH, through its subsidiary EP Slovakia BV, acquired 50% of Slovak Power Holding BV, which in turn owns 66% of Slovenské Elektrárne.

Křetínský subsequently acquired a stake in Slovenské Elektrárne's power plants from the Italian company Enel (which owns the remaining 50 percent of Slovak Power Holding BV). He has an option for an additional 33 percent of the shares after the start-up of the two units of the Mochovce nuclear power plant, which is still under construction. The third unit is already in the test phase, but the cost of the whole project has become prohibitive, bringing Slovenské Elektrárne to the brink of bankruptcy and swelling its debt to over €4 billion.

Enel and EPH agreed in 2020 to provide additional loans of €570 million and €200 million respectively to the company. By acquiring a further 33% of Slovenske Elektrárne (between 2026 and 2032), EPH would also take on the obligation to repay the loans of its former partner Enel, to the tune of €1.3 billion.

It is not yet clear how EPH will handle its other debts – nearly €1 billion – once it takes control of the Slovak company. At the moment, Křetínský's holding company has not yet incorporated Slovenské Elektrárne, so its debt has not yet been included in the company's results.

So while Křetínský speculates in other sectors with energy revenues, his companies are increasingly indebted and facing uncertain times. The gas infrastructure is under threat, the coal-fired power plants too – and a lot depends on political decisions at European level.

The old business model, made viable by gas revenues that were considered risk-free and highly regulated until spring 2022, now looks shaky. But Křetínský seems to thrive on uncertainty, as evidenced by the opacity of the Cypriot and Luxembourg companies where the profits of his companies would appear to land.

An opaque ownership structure

The island of Aphrodite is home to a veritable nest of Russian dolls, thanks in particular to the opacity guaranteed by Cypriot company regulations.

EPH Holding is currently 44%-owned by Patrik Tkáč's holding company J&T Energy, with the remaining 56% owned by EP Corporate Group – itself owned by Křetínský. Founded in 2019, this other Czech company has not yet issued an annual balance sheet. According to Slovakian records, EP Corporate Group is 89.29%-owned by EP Investment Sarl, with the remaining 10.71% owned by the Cypriot company Tilia Cordata (the Latin name for lime tree). However, the latter is not mentioned in EPH's annual balance sheet, and Křetínský appears to be its ultimate beneficial owner, despite owning only 7.44% of the company.

The information contained in the Czech company register – i.e., that EP Corporate Group was 100%-owned by EP Investment Sarl until November – therefore does not correspond to what is contained in the Luxembourg and Slovak registers. In several Luxembourg annual reports, it appears that the remaining 90.56% of Tilia Cordata's shares are held by "senior EPH executives who have invested in the company". This has been confirmed by company spokesman Daniel Častvaj: "The ultimate beneficiaries of Tilia Cordata, apart from Daniel Křetínský, are simply selected members of EPH management."

Sleight of hand

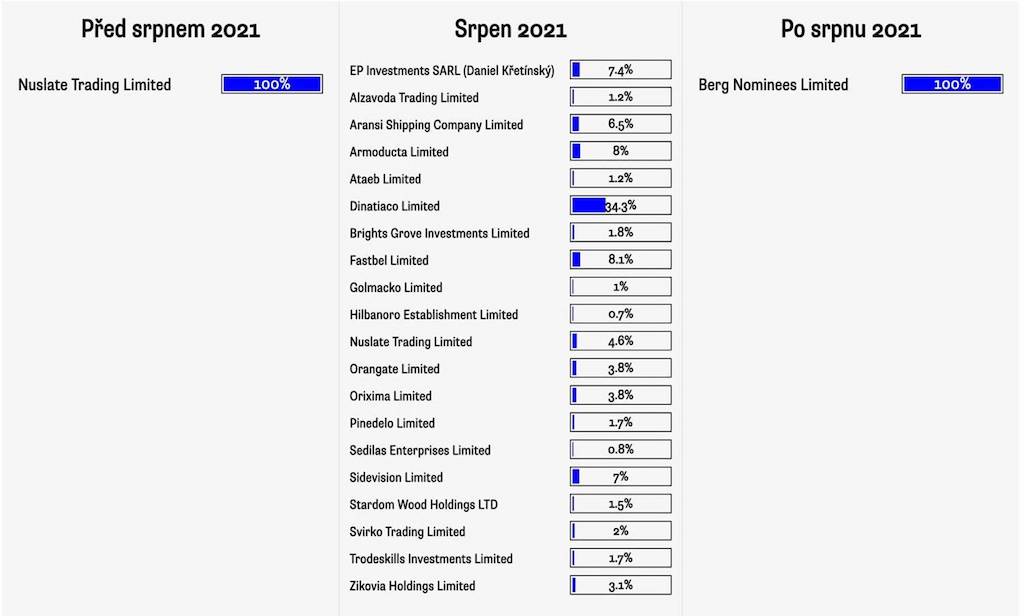

In the past, Tilia Cordata was controlled by another Cypriot company, Nuslate Trading Limited. Then in August 2021 the company was restructured in a peculiar way: the single manager was replaced by twenty different companies, each with a separate shareholding.

The shareholding in the company owned by Daniel Křetínský – through EP Investment Sarl – is the only one that can be established from public sources. Eighteen of these companies are Cypriot, and one leads to the British Virgin Islands.

It is through these companies that EPH's "top managers" then own shares in Tilia Cordata. When asked who is behind the companies, Daniel Častvaj only says: "The companies mentioned are 'special-purpose vehicles' through which the individual managers hold their shares. This is not unusual."

Their boards are mostly made up of Cypriot citizens. Only two EPH board members sit on them. There are also three Slovak managers, whose names have appeared in the past in investigations concerning shell companies. One other thing connects them: they are all involved in the Cypriot company Bridge Global Solutions Ltd, which runs letterbox companies for J&T Energy, the holding company of Patrik Tkáč (him again).

As of September 2021, Tilia Cordata returned to a simpler system of management – under the leadership of Berg Nominees Ltd, a Cyprus-based shell company whose shareholders are by definition anonymous. This lack of transparency seems to please Křetínský and his "senior managers".

No information on Berg Nominees Ltd is present in the Slovak register of public-sector partners. The EPH spokesperson denies that the company has violated its legal obligations, which is confirmed by a specialist lawyer consulted for this investigation. But in the end, is it appropriate for a holding company of EPH's size and importance to hide its real shareholders? Častvaj remains unmoved: "Of course [it is]. The banks and regulators involved have detailed information and they have no problem with it. They certainly don't consider it 'opaque'."

In this ballet of Russian dolls, where companies own each other and hidden shareholders move from one board to another, it can be hard to find what you came looking for. So the Russian gas revenues amassed by EPH seem safe, for now.